Editor: Asia Pacific Elite Wealth Management Institute

Outlook for Global Economic Cycle and Major Types of Assets Trend in 2021

Current Global Economic Cycle – From “Recovery” to “Growth”

In 2020, COVID-19 pandemic swept the world, causing the global economy to hit the worst recession since World War II. According to the Economic Outlook Report of IMF in January 2021, it is estimated that the global GDP growth rate will decline by 3.5% in 2020. However, with the unprecedented stimulus of monetary and fiscal policies introduced by central banks and governments around the world, as well as the gradual implementation of vaccination, IMF estimates that the global GDP will rebound by 5.5% in 2021, reaching the highest growth rate since the 1970s.

So, from recession to rebound, which stage is the current global economic cycle in? According to the survey data of economists by the Centre for European Economic Research (ZEW) and China Economic Monitoring and Analysis Center, we have constructed an economic cycle’s clock. It divides the economic cycle into four stages from two dimensions, namely “economic status assessment” and “future economic expectation”, so as to accurately locate the current economic cycle position.

The latest statistics shows that China’s current economic situation has turned positive in the fourth quarter of 2020, and has officially entered the “growth” stage. The United States and the Eurozone were in the “recovery” stage in February 2021, but the current economic situation of the United States is definitely moving towards the “growth” stage. While the Eurozone has been hovering in place since September 2020, which is obviously affected by the second wave of pandemic, and at the same time lacks the fiscal stimulus like that of the United States. If defined in terms of -100~0, the United States is currently at -47 and the Eurozone is at -74. Overall, the economic dynamism of the two largest economies, the United States and China, which account for about 40% of the global economy, shows that the global economic cycle is moving towards a “growth” stage.

Figure 1: China’s economic cycle has entered a “growth” stage, while Europe and the United States are in a “recovery” stage

Source: Bloomberg, 2021/3/10

Note:

(1) The economic cycle’s clocks of the United States and the Eurozone use data from the ZEW survey. The survey interviewed more than 300 experts from banks, insurance companies and financial departments in specific industries around the world to evaluate the financial market and economic condition. If the index is greater than 0, it means that the market view is optimistic, and if it is less than 0, it means that the view is pessimistic.

(2) The economic cycle’s clock of China uses data surveyed by China Economic Monitoring and Analysis Center under the National Bureau of Statistics. The survey interviewed 100 Chinese economists to evaluate the economic situation. The index takes 100 as the line of prosperity, with higher than 100 representing economic expansion and lower than 100 representing economic contraction. In order to be consistent with the economic cycle’s clocks in Europe and the United States, this chart reduces the data interval by 100 and adjusts it from 100~200 to 0~100.

Outlook for Global Major Types of Assets – Dominating the Market in a Cyclical Way, Does Interest Rate Fluctuation Bring Disturbance?

In November 2020, Pfizer launched the first COVID-19 vaccine, and after Biden was elected as the United States president, the expectation of a strong recovery of the global economy made “reflation trade” begin to dominate the global financial market. Major types of assets that are sensitive to the economic cycle started to rise continuously in the long-run. Specifically, during the two months from November 2020 to the end of the year, the Dow Jones Industrial Average, cyclical stock, equity stock and small cap in the U.S. stock market outperformed the technology sector. The rapid increase in inflation expectations also led to a higher yield of long-term U.S. Treasury bonds and commodities; while the U.S. dollar index continued to decline due to the rising risk sentiments.

After the Democratic Party of the United States won the Senate in January 2021, the Blue Wave further pushed forward the trend of reinflation transactions. However, since mid-February, the yield of the 10-year U.S. Treasury bonds has accelerated upward. Expectations of adjustment of stock valuation and early tightening of ultra-loose monetary policy have plunged the risky assets into turmoil and uncertainty. The key question for investors now is: Will the Federal Reserve tighten monetary policy ahead of time? Can Biden’s infrastructure plan be successfully implemented? Can vaccines normalize the global economy? Will there be another crash in the stock market?

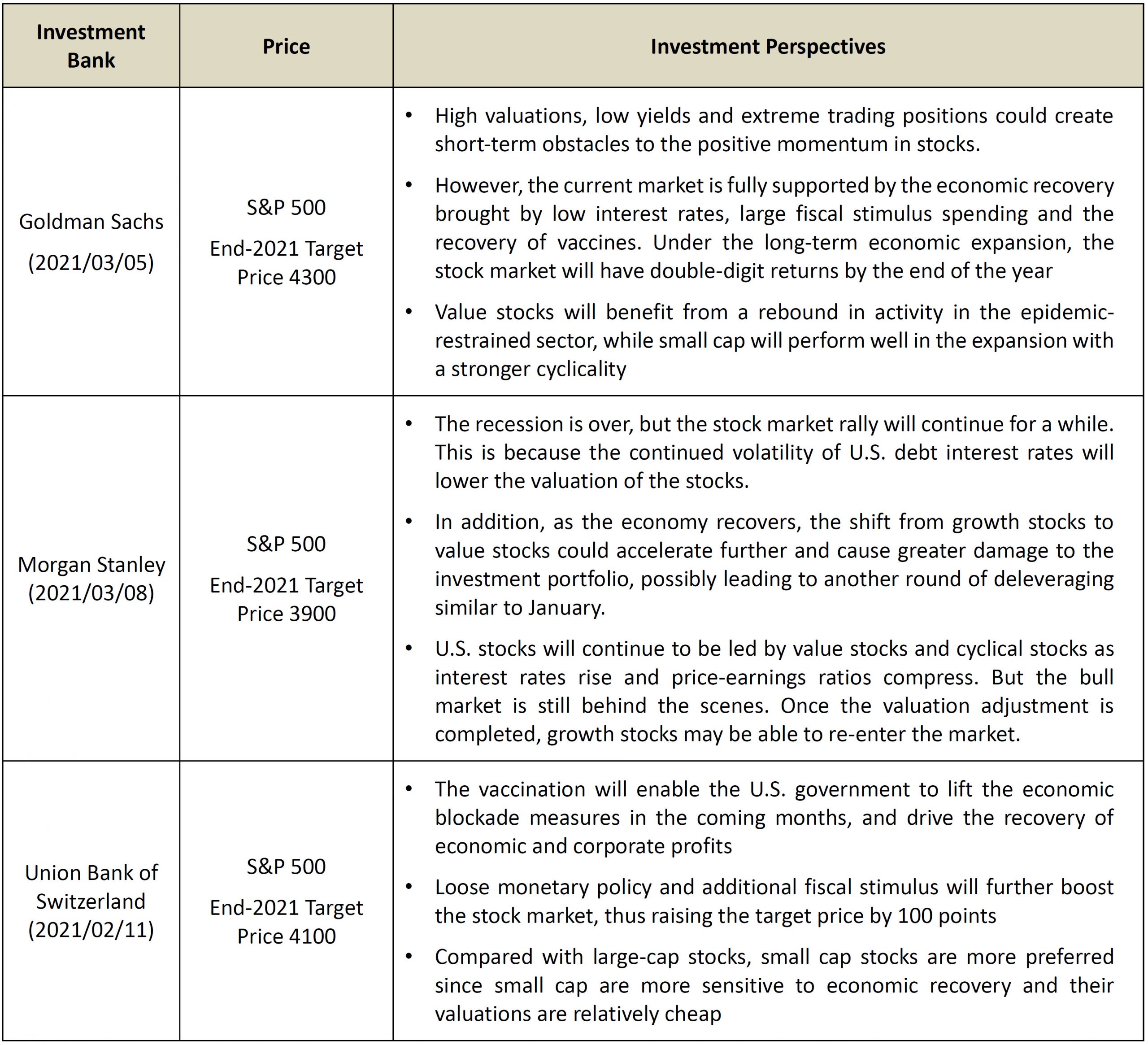

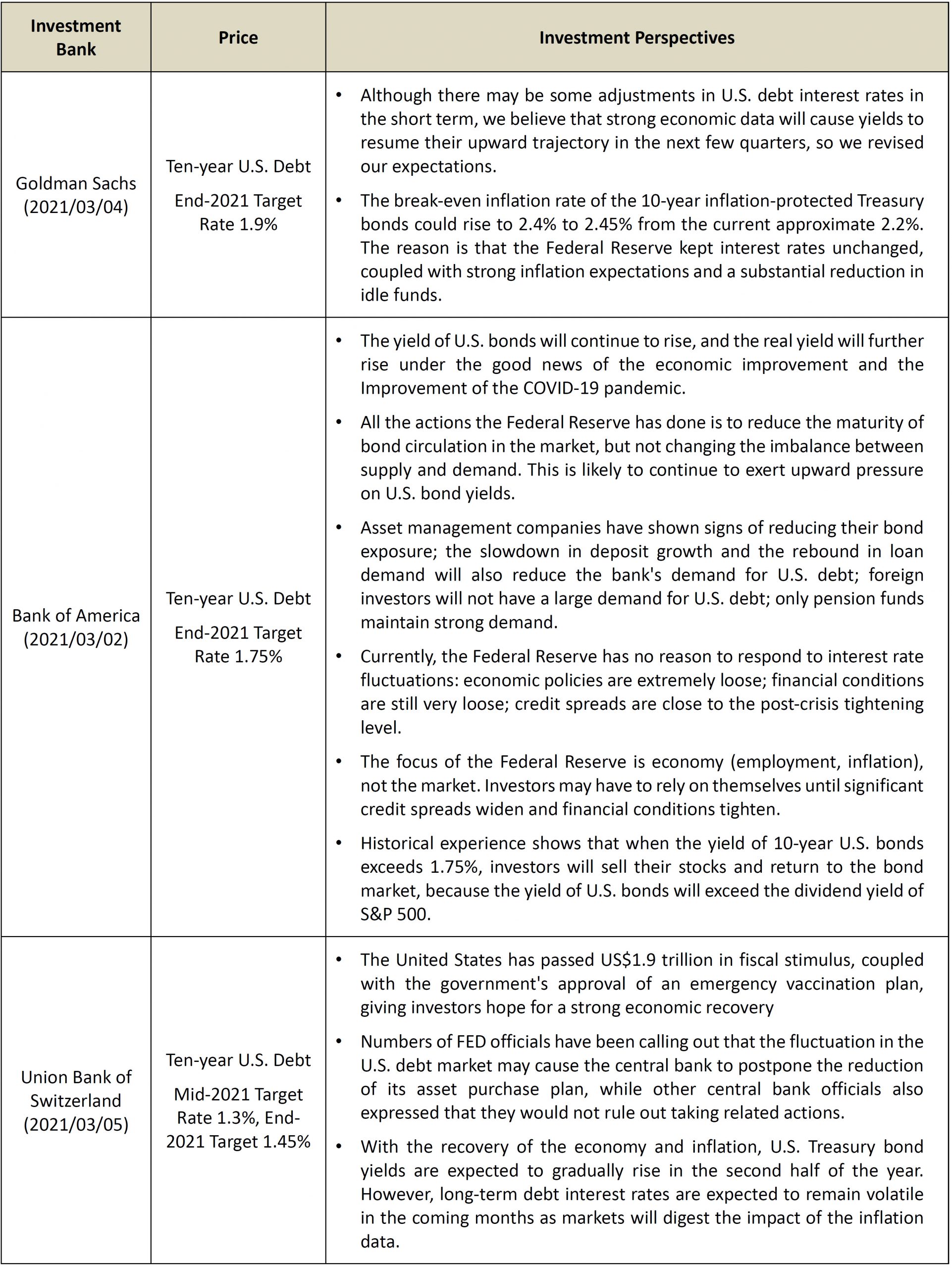

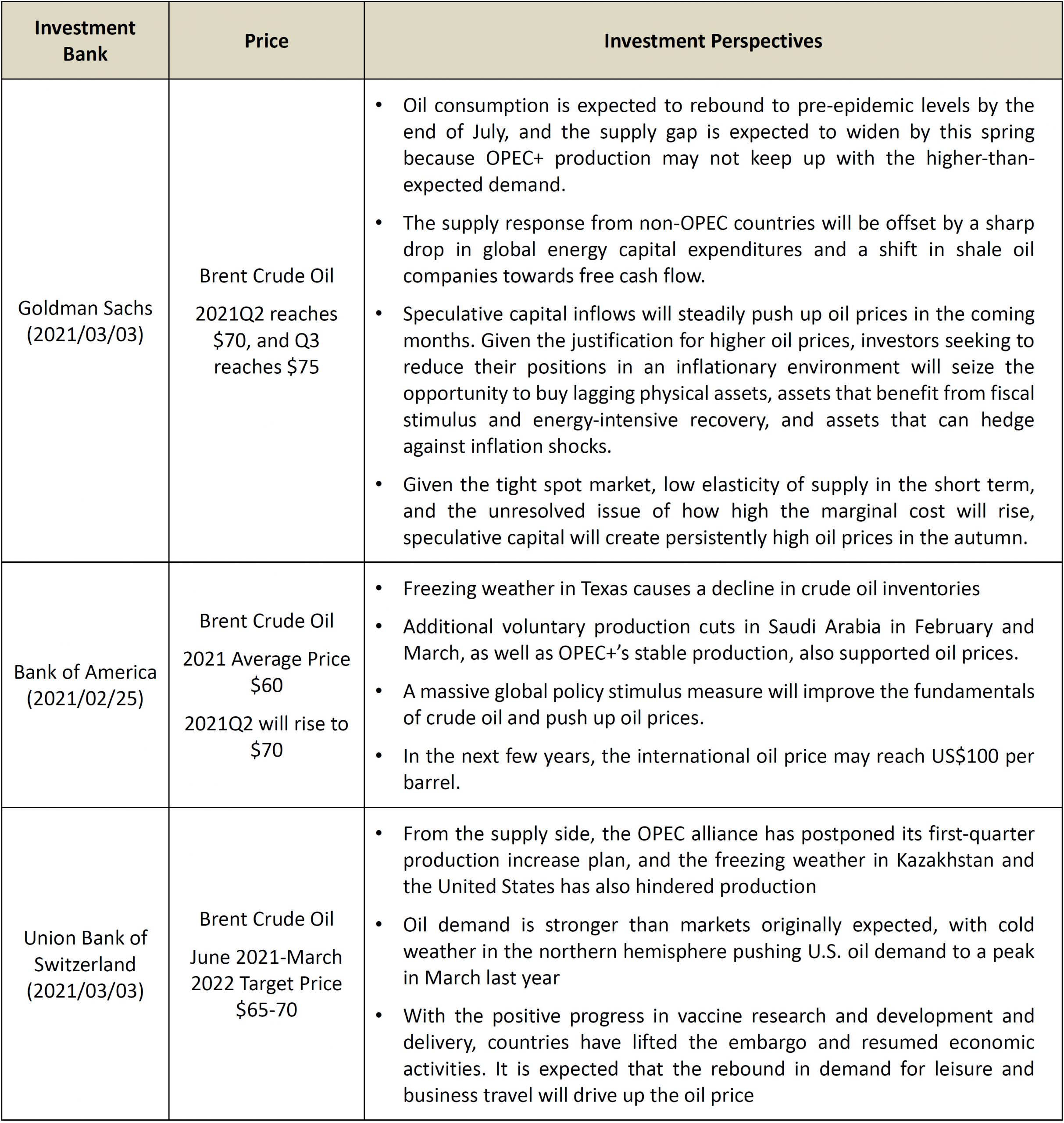

The following is the view of major international investment banks on major types of assets since the beginning of the year, hoping to help investors find out the answers to these key questions and better grasp the opportunities and risks of investment layout in 2021.